![]()

![]()

StatsPAI is for empirical researchers who would normally jump between Stata, R, and Python. Its goal is to make common Stata/R econometrics and causal-inference workflows feel native in Python: load a dataset, estimate a model, inspect diagnostics, export tables, and hand the result to an agent or notebook without leaving one API.

It is meant to be a practical replacement path for new Python-first work:

- Stata-style routines:

regress,ivregress,reghdfe,csdid,rdrobust,synth,psmatch2,outreg2. - R-style routines:

lm,fixest,did,rdrobust,Synth,DoubleML,MatchIt,modelsummary,broom. - Python-native outputs:

.summary(),.tidy(),.plot(),.to_latex(),.to_docx(),.to_agent_summary()where supported by the result object. - Companion Stata tooling: our own

stata-codecan work with StatsPAI so agents can understand existing Stata workflows, translate them into Python, and cross-check results more smoothly. - Companion skill repos:

Auto-Empirical-Research-Skills,AER-Skills,Awesome-Journal-Skills, andPaper-WorkFlowcan work alongside StatsPAI and an agent as the methods, journal, manuscript, and reproducibility skill layer.

StatsPAI is not a promise that every Stata/R command is bit-for-bit identical.

When exact external parity matters, use the validation_status metadata,

the reference-parity tests, and sp.cross_validate to see what has been

certified for that estimator.

pip install statspaiThen:

import statspai as sp

print(sp.datasets.list_datasets()[["name", "design", "n_obs"]].head())StatsPAI ships teaching datasets such as Card (1995), Callaway-Sant'Anna

mpdta, Lee (2008) RD, LaLonde/NSW, and California Proposition 99. The examples

below run offline after installation.

At a glance: 1,139 registered functions across 87 submodules; 339k LOC (core) + 182k LOC (tests). Run python scripts/registry_stats.py to reproduce these numbers.

| What you used before | Stata / R examples | StatsPAI entry point |

|---|---|---|

| OLS / robust SE | reg y x, vce(robust) / lm() + sandwich |

sp.regress(..., robust="hc1") |

| IV / 2SLS | ivregress 2sls / AER::ivreg() |

sp.ivreg("y ~ (d ~ z) + x", data=df) |

| High-dimensional FE | reghdfe / fixest::feols() |

`sp.feols("y ~ x |

| Staggered DiD | csdid / did::att_gt() |

sp.callaway_santanna() + sp.aggte() |

| Regression discontinuity | rdrobust / rdrobust::rdrobust() |

sp.rdrobust() |

| Synthetic control | synth / Synth::synth() |

sp.synth() |

| Matching / PSM | psmatch2 / MatchIt |

sp.psmatch2() and matching helpers |

| Publication tables | outreg2, esttab / modelsummary |

sp.outreg2(), sp.modelsummary() |

StatsPAI is meant to be the broad Stata/R-style workbench for applied empirical research, not only a single modeling family.

| Package | Best fit | Where StatsPAI is different |

|---|---|---|

causallib |

Observational causal inference with a scikit-learn-style workflow: IPW, matching, standardization, doubly robust estimation, and evaluation. | StatsPAI is broader for Stata/R migration: OLS, IV, high-dimensional FE, DiD, RD, synthetic control, matching, diagnostics, validation metadata, and publication-table export in one API. |

CausalPy |

Bayesian causal analysis for quasi-experimental settings, built around PyMC models, uncertainty, and visual diagnostics. | StatsPAI prioritizes familiar Stata/R econometrics commands, frequentist workflows, cross-language parity evidence, bundled teaching datasets, and agent-ready result summaries. |

Use causallib when you mainly want sklearn-style treatment-effect pipelines.

Use CausalPy when you want Bayesian causal modeling in PyMC. Use StatsPAI when

you want one Python package to replace the everyday Stata/R empirical workflow.

The outputs below are rounded from the bundled examples in this repository using StatsPAI 1.20.0.

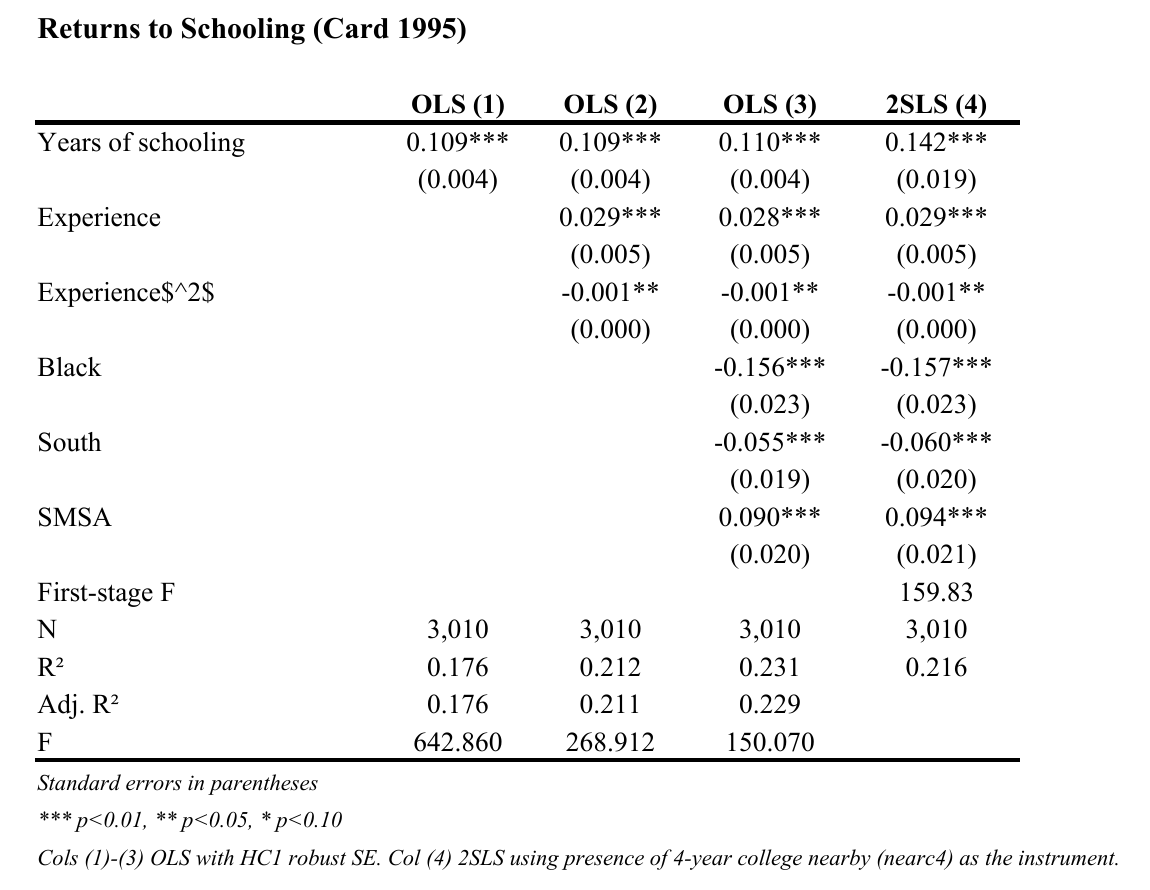

Question: how much higher is log wage for one more year of schooling in the Card (1995) teaching dataset?

import statspai as sp

card = sp.datasets.card_1995()

ols = sp.regress(

"lwage ~ educ + exper + expersq + black + south + smsa",

data=card,

robust="hc1",

)

print(ols.summary())Result:

Model: OLS

Dependent Variable: lwage

Coefficient Std. Error t-statistic P>|t|

Intercept 4.8388 0.0637 76.0131 0.0000

educ 0.1100 0.0041 26.5543 0.0000

exper 0.0283 0.0054 5.2742 0.0000

expersq -0.0005 0.0002 -2.2132 0.0270

black -0.1561 0.0231 -6.7571 0.0000

south -0.0554 0.0193 -2.8636 0.0042

smsa 0.0905 0.0205 4.4214 0.0000

R-squared: 0.2307

Read it like a Stata/R regression table: in this replica, one additional year

of schooling is associated with about 0.110 higher log wage, before dealing

with endogeneity. Adding the standard Card (1995) controls (experience and

its square, race, region, SMSA) lifts R² from 0.210 to 0.231 and the

educ coefficient is essentially unchanged — the small attenuation from

classical measurement error in educ persists and motivates the IV in

example 2.

Question: instrument education with proximity to a four-year college (nearc4).

import statspai as sp

card = sp.datasets.card_1995()

iv = sp.ivreg(

"lwage ~ (educ ~ nearc4) + exper + expersq + black + south + smsa",

data=card,

)

print(iv.summary())Result:

Model: IV-2SLS

Dependent Variable: lwage

Coefficient Std. Error t-statistic P>|t|

educ 0.1418 0.0188 7.5606 0.0000

Model Diagnostics:

First-stage F (educ): 159.8305

Partial R2 (educ) : 0.0505

Hausman p-value : 0.0322

StatsPAI prints the coefficient and the diagnostics you would usually collect with separate post-estimation calls.

Question: what is the average minimum-wage effect on teen employment in the

Callaway-Sant'Anna mpdta example?

import statspai as sp

mp = sp.datasets.mpdta()

gt = sp.callaway_santanna(

data=mp,

y="lemp",

t="year",

i="countyreal",

g="first_treat",

)

overall = sp.aggte(gt, type="simple", bstrap=False)

print(overall.summary())Result:

Callaway and Sant'Anna (2021) - aggte[simple]

ATT: -0.032977

Std. Error: 0.005493

95% CI: [-0.043742, -0.022211]

P-value: 0.0000

Observations: 2,500

The headline estimate is negative and statistically precise in this bundled replica.

Question: is there an incumbent advantage at the zero-margin cutoff in the Lee (2008) Senate election design?

import statspai as sp

lee = sp.datasets.lee_2008_senate()

rd = sp.rdrobust(data=lee, y="voteshare_next", x="margin", c=0)

print(rd.summary())Result:

Sharp RD Estimation

RD Effect: 0.061599

Std. Error: 0.022662

95% CI: [0.017183, 0.106015]

P-value: 0.0066

Bandwidth H: 0.042287

N Effective Left: 440

N Effective Right: 443

The robust bias-corrected RD estimate is about 0.062 vote-share points.

Question: how did California's Proposition 99 affect cigarette sales?

import statspai as sp

prop99 = sp.datasets.california_prop99()

sc = sp.synth(

data=prop99,

outcome="cigsale",

unit="state",

time="year",

treated_unit="California",

treatment_time=1989,

)

print(sc.summary())Result:

Synthetic Control Method

ATT: -13.085166

Std. Error: 4.164718

95% CI: [-21.247862, -4.922469]

P-value: 0.0789

Active donor weights:

Montana 0.8420

Nevada 0.1580

The estimate says California consumed about 13 fewer packs per capita after the intervention in this replica.

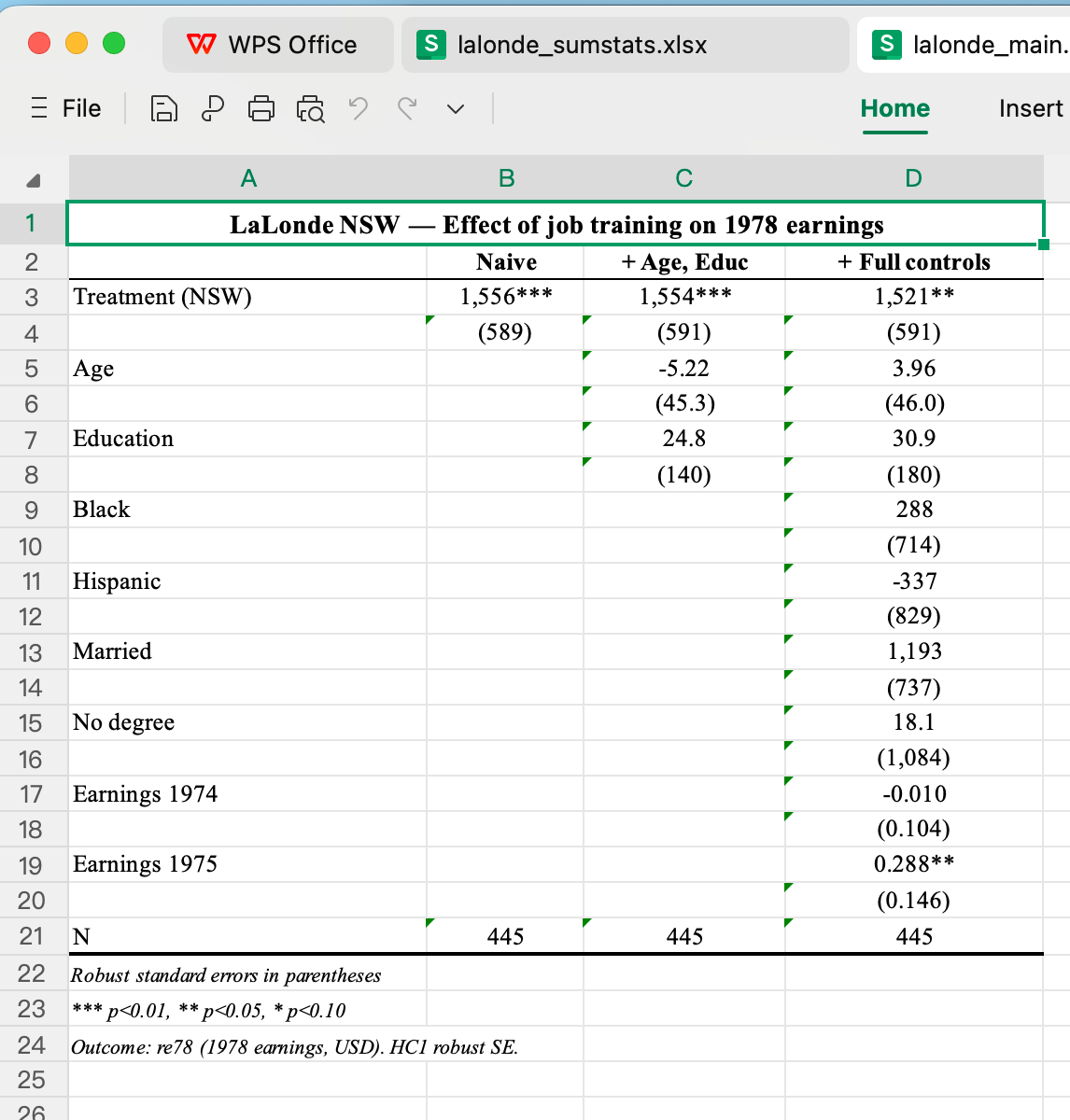

Every result object ships with Stata-style and R (modelsummary/broom)

exporters. One call drops a multi-sheet .xlsx or a Word table that you can

hand to a co-author.

sp.outreg2(r1, r2, filename="results.xlsx") # Excel, Stata-style

sp.modelsummary(r1, r2, output="table.docx") # Word, modelsummary-style

The screenshots above are the .xlsx output of sp.outreg2 on the Card (1995)

OLS + IV pair and the LaLonde/NSW propensity-score regression. Each sheet

contains the coefficient table, model-fit statistics, and significance stars

in the format your journal template expects.

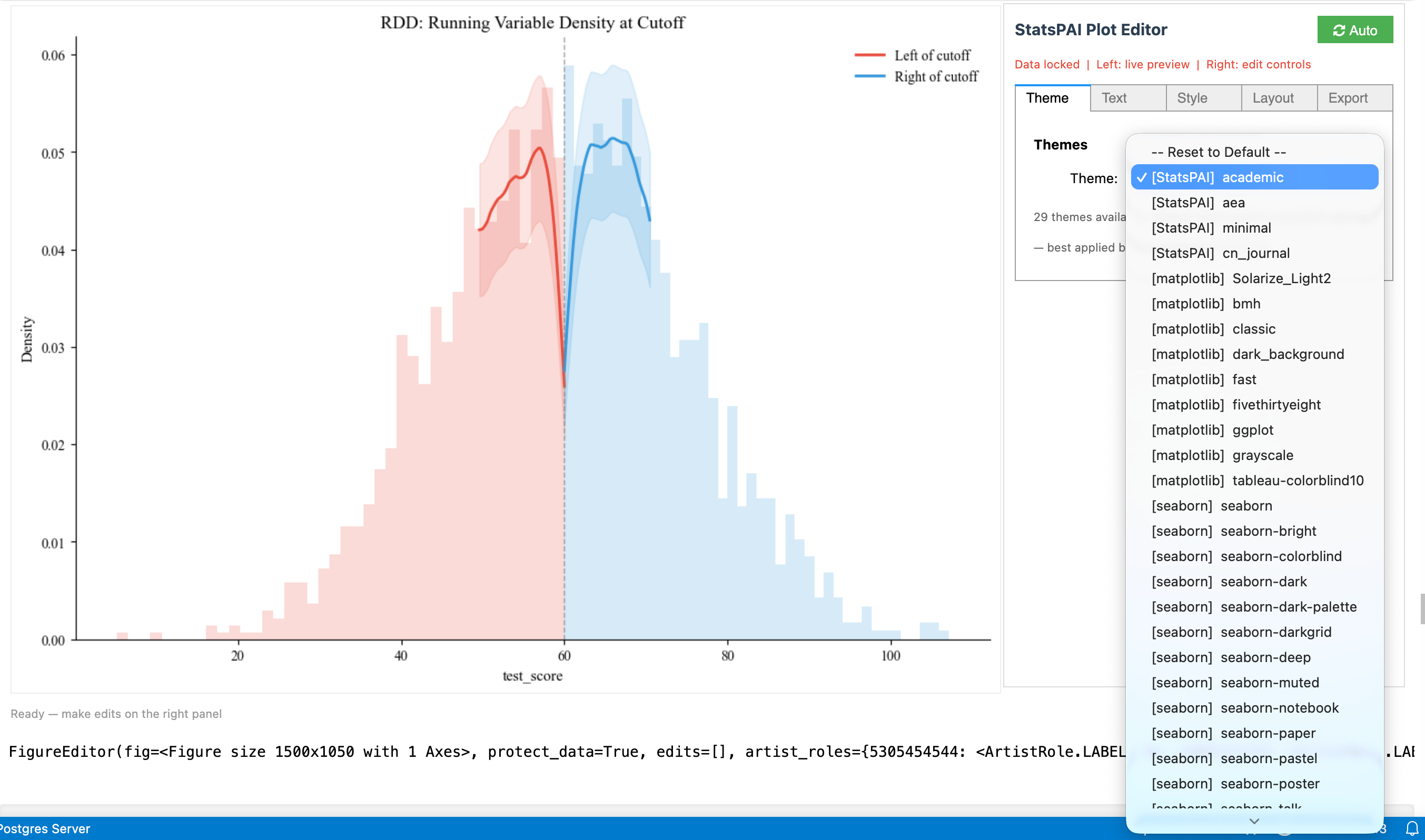

If you miss Stata's Graph Editor, use sp.interactive(fig) on any matplotlib

figure returned by StatsPAI. It opens a Jupyter editing panel with a live

preview, so beginners can adjust a figure without learning every matplotlib

option first.

What it is for:

- change titles, labels, fonts, colors, markers, line widths, grids, legends, axis limits, figure size, and export DPI;

- switch among publication-oriented themes, including academic, ggplot-like, FiveThirtyEight-style, and dark presentation styles;

- keep the data layer protected while editing cosmetic elements;

- export reproducible Python code for the edits, so the final figure can be regenerated from a script instead of being only a manual screenshot.

import statspai as sp

mp = sp.datasets.mpdta()

gt = sp.callaway_santanna(data=mp, y="lemp", t="year",

i="countyreal", g="first_treat")

agg = sp.aggte(gt, type="dynamic", bstrap=False)

fig, ax = sp.ggdid(agg)

editor = sp.interactive(fig) # edit the plot in Jupyter

print(editor.generate_code()) # copy reproducible matplotlib edits

The screenshot above shows the intended workflow: preview on one side, editing controls on the other, and code export for reproducibility.

import statspai as sp

card = sp.datasets.card_1995()

r1 = sp.regress(

"lwage ~ educ + exper + expersq + black + south + smsa",

data=card,

robust="hc1",

)

r2 = sp.ivreg("lwage ~ (educ ~ nearc4) + exper + expersq + black + south + smsa", data=card)

print(r1.summary()) # human-readable table

print(r1.tidy().head()) # broom-style dataframe

sp.modelsummary(r1, r2, output="table.docx") # Word table

sp.outreg2(r1, r2, filename="results.xlsx") # Stata-style exportUseful docs:

- Getting started

- Cookbook

- Choosing an IV estimator

- Choosing a DID estimator

- Choosing an RD estimator

- Migrating from R to StatsPAI

- Exporting regression tables

StatsPAI has a large API surface, so validation status matters.

import statspai as sp

print(sp.describe_function("ivreg")["validation_status"])

print(sp.list_functions(validation_status="certified")[:5])Use the validation metadata to distinguish:

- certified functions with external numerical evidence;

- validated functions with internal or published-reference checks;

- API-stable functions whose interface is stable but whose exact Stata/R parity may be design-dependent;

- experimental functions for frontier workflows.

Agent-facing metadata is available through sp.list_functions(),

sp.describe_function(), and sp.function_schema().

The validation tier above has a richer, auditable backing: a parity index

where every verified function records what it was aligned against, to what

tolerance, on which test, and how closely it matched. Each row traces to a

committed test artifact (the pinned StatsPAI ↔ R ↔ Stata harness, version-locked

via renv.lock + per-run provenance) — nothing is asserted from memory.

import statspai as sp

sp.parity_status("feols")

# {'status': 'bit-exact', 'reference': 'fixest::feols',

# 'reference_versions': {'R': '...4.5.2...', 'fixest': '0.14.0'},

# 'tolerance': 'rel_est<=1e-06, rel_se<=1e-06', 'headline': {...}, 'test': [...]}

sp.parity_summary() # honest coverage counts (verified vs unverified)

sp.parity_matrix(status="bit-exact")Grades: bit-exact (machine tolerance vs a named R/Stata reference), aligned

(documented looser tolerance), analytical-only (recovers a known DGP truth),

external-replication (published-paper numbers), and unverified (registered

but no parity evidence attached yet — the honest gap). The full,

auto-generated matrix is published at

docs/parity.md.

Release notes live outside the README:

- CHANGELOG.md for the full version history.

- Docs changelog page for the rendered documentation site.

The README is intentionally focused on first-time users.

StatsPAI is under JOSS review. Reviewers can start with:

If you use StatsPAI in research, cite the package and the underlying method

papers for each estimator. sp.citation() returns the package citation, and

many result objects expose estimator-level citation helpers.

@software{wang2026statspai,

author = {Wang, Biaoyue and Rozelle, Scott},

title = {StatsPAI: Validation-Tiered Causal Inference and

Econometrics Workflows for Python},

year = {2026},

version = {1.20.0},

url = {https://github.com/brycewang-stanford/StatsPAI}

}MIT. See LICENSE.